1. What is the Industrial Battery Market Overview – definition, scope, and significance?

The Industrial Battery Market encompasses the production, distribution, and application of rechargeable and non‑rechargeable batteries used in heavy‑duty sectors such as telecom, mining, marine, and large‑scale industrial equipment. It covers a broad range of chemistries—including lead‑acid, lithium‑based, and nickel‑based solutions—tailored for high‑capacity, long‑life, and robust performance. The market is significant because reliable power storage underpins critical operations, enhances equipment uptime, and supports the transition to greener energy systems across multiple industries.

2. What are the main drivers, restraints, challenges, and opportunities shaping the Industrial Battery Market?

Key drivers include rising demand for backup power in data centers, increased automation in manufacturing, and the shift toward electrified marine and mining equipment. Restraints arise from high upfront capital costs and strict safety regulations governing battery handling. Challenges involve supply‑chain constraints for raw materials like lithium and nickel, as well as the need for advanced thermal‑management technologies. Opportunities exist in developing high‑energy‑density lithium solutions, offering recycling services, and expanding into emerging markets where grid reliability remains limited.

3. Which growth trends are currently influencing the Industrial Battery Market?

Current trends feature a rapid adoption of lithium‑based batteries due to their superior energy density and lighter weight, while legacy lead‑acid systems are being upgraded with advanced valve‑regulated designs. The market also sees integration of smart‑monitoring IoT platforms that provide real‑time health diagnostics. Furthermore, modular battery architectures are gaining traction, allowing scalable deployments for both stationary UPS applications and mobile industrial equipment.

4. How did COVID‑19 impact the Industrial Battery Market and what is the recovery trajectory?

The pandemic disrupted supply chains for raw materials and delayed capital‑intensive projects, leading to a temporary slowdown in new installations. However, the surge in remote work and increased reliance on data centers created heightened demand for uninterrupted power supplies, accelerating UPS battery orders. Recovery is now steady, with market confidence restored as manufacturers resume full‑capacity production and customers prioritize resilience in critical infrastructure.

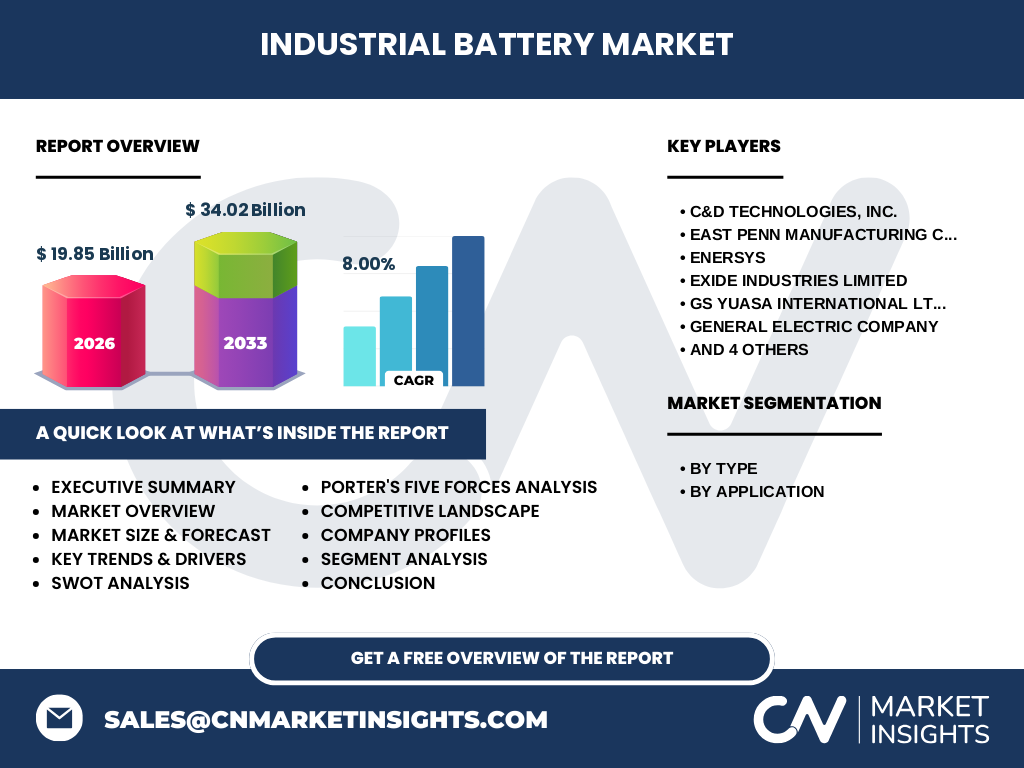

5. Who are the major competitors and what is the state of consolidation in the Industrial Battery Market?

Prominent players include C&D Technologies, Inc., East Penn Manufacturing Company, EnerSys, Exide Industries Limited, GS Yuasa International Ltd., General Electric Company, LG Chem, Panasonic Corporation, Robert Bosch GmbH, and Saft Groupe SA. The competitive landscape is characterized by strategic partnerships, joint ventures for technology sharing, and selective acquisitions aimed at expanding product portfolios and geographic reach, indicating a moderate level of consolidation.

6. What are the key findings presented in the Executive Summary of the Industrial Battery Market?

The Executive Summary highlights a market valued at $19.85 billion in 2026, projected to reach $34.02 billion by 2033, reflecting a CAGR of 8.0 %. Growth is propelled by expanding data‑center infrastructure, electrification of heavy equipment, and evolving battery‑management systems. Lead‑acid remains the volume leader, while lithium‑based batteries capture the fastest growth segment. Regional demand is strongest in North America and Asia‑Pacific, with emerging opportunities in Africa and Latin America.

7. What is the forecast for the Industrial Battery Market from 2025 to 2032?

Based on the provided CAGR of 8 %, the market is expected to maintain steady expansion throughout the 2025‑2032 horizon. Revenue will progress from a mid‑2020s baseline toward the 2033 projection of $34.02 billion, driven by continued investment in renewable‑energy storage, increased UPS deployments, and broader adoption of lithium chemistries across industrial sectors. The forecast underscores robust demand across all major applications.

8. How is the Industrial Battery Market sized and shared by type and application segments?

Segmentation by type divides the market into lead‑acid, lithium‑based, and nickel‑based batteries. Lead‑acid accounts for the largest volume due to its cost advantage in UPS and backup power, while lithium‑based batteries command the highest growth rate because of superior performance in telecom, data‑communication, and mobile mining equipment. Nickel‑based solutions serve niche applications requiring high discharge rates. By application, the market splits among telecom & data communication, industrial equipment, UPS/backup, mining, and marine sectors, each contributing to the overall market footprint.

9. What is the global Industrial Battery Market size and share by region?

The global market reached $19.85 billion in 2026 and is forecast to expand to $34.02 billion by 2033. While precise regional shares are not enumerated, the market’s growth is anchored by strong demand in North America and Asia‑Pacific, where industrial automation and data‑center construction are most intense. Europe contributes a steady share, supported by stringent emission regulations that favor battery‑backed power solutions.

10. How does the Industrial Battery Market perform across different regions?

In North America, robust industrial automation and extensive UPS deployments drive market momentum. Asia‑Pacific, led by China, India, and South Korea, experiences rapid growth due to large‑scale manufacturing, expanding telecom networks, and governmental incentives for clean‑energy storage. Europe’s performance is bolstered by strict environmental policies and investment in offshore wind‑farm backup systems. Emerging regions such as Latin America and Africa are beginning to adopt industrial battery solutions to mitigate grid unreliability.

11. Which leading companies dominate the Industrial Battery Market and what are their strategic approaches?

Key players include C&D Technologies, East Penn, EnerSys, Exide, GS Yuasa, GE, LG Chem, Panasonic, Bosch, and Saft. Strategies employed encompass diversification into lithium chemistries, development of integrated battery‑management platforms, expansion of global service networks, and collaborations with OEMs for customized solutions. Several firms are also investing in recycling infrastructure to address raw‑material sustainability and regulatory compliance.

12. What does Porter’s Five Forces reveal about the Industrial Battery Market?

• Threat of new entrants: Moderate, due to high capital requirements and stringent safety standards.

• Bargaining power of suppliers: High, driven by limited sources of lithium, nickel, and cobalt.

• Bargaining power of buyers: Growing, as industrial customers demand cost‑effective, high‑performance solutions.

• Threat of substitutes: Low to moderate; alternative energy storage technologies exist but lack the proven reliability of batteries for critical applications.

• Industry rivalry: Intense, with multiple established players competing on technology, price, and service.

13. What are the main strengths, weaknesses, opportunities, and threats identified in the SWOT analysis?

Strengths: Established technology base, broad application spectrum, and increasing demand for grid‑resilient power.

Weaknesses: High upfront costs for advanced chemistries and dependence on raw‑material supply.

Opportunities: Expansion of lithium‑based product lines, rollout of circular‑economy recycling programs, and penetration into underserved emerging markets.

Threats: Raw‑material price volatility, regulatory changes concerning battery safety and disposal, and competitive pressure from alternative storage solutions.

14. How is the value chain of the Industrial Battery Market structured?

The value chain begins with raw‑material extraction (lithium, lead, nickel), followed by component manufacturing (electrodes, separators), cell assembly, module integration, and system integration for specific applications. Subsequent stages include distribution, installation, after‑sales service, and end‑of‑life recycling. Value‑added services such as predictive maintenance, remote monitoring, and battery‑as‑a‑service models are increasingly embedded within the chain.

15. What investment insights can be drawn for stakeholders considering the Industrial Battery Market?

Investors should prioritize companies with strong lithium‑technology pipelines and diversified regional footprints. Funding recycling initiatives can mitigate raw‑material risk and align with ESG goals. Strategic investments in IoT‑enabled battery‑management platforms offer high‑margin growth. Finally, joint ventures that combine battery manufacturers with equipment OEMs can secure long‑term contracts and enhance market defensibility.

16. What are the concluding takeaways from the Industrial Battery Market analysis?

The Industrial Battery Market is on a clear growth trajectory, moving from a $19.85 billion base in 2026 to an anticipated $34.02 billion by 2033, propelled by an 8 % CAGR. Lithium‑based solutions are reshaping the landscape, while legacy technologies remain relevant in cost‑sensitive segments. Regional dynamics favor North America and Asia‑Pacific, and strategic focus on supply‑chain resilience, recycling, and digital services will differentiate market leaders.

17. Which research methodology was applied to develop this market report?

The study employed a mixed‑method approach, combining primary interviews with industry executives, secondary data extraction from company filings, trade publications, and reputable databases. Quantitative estimates were derived using a top‑down market sizing technique, calibrated against the provided baseline figures. Forecasting utilized a compound‑annual‑growth model aligned with the stated 8 % CAGR.

18. What is the scope of this research and its limitations?

The scope covers global industrial battery applications, focusing on type and end‑use segmentation, and includes key competitive, financial, and technological analyses up to 2033. Limitations stem from the reliance on publicly available data and the exclusion of confidential pricing or market‑share specifics beyond the provided aggregate figures.

19. Which key companies have announced recent developments in the Industrial Battery Market?

Recent activities include C&D Technologies launching a high‑power lithium‑ion UPS series; East Penn unveiling an advanced lead‑acid valve‑regulated battery for marine use; EnerSys expanding its global service network; Exide introducing a recycling‑focused program in Asia; GS Yuasa partnering with a telecom OEM for customized battery packs; GE integrating battery storage in its renewable‑energy solutions; LG Chem releasing a next‑generation lithium‑ferro‑phosphate cell; Panasonic scaling production of solid‑state batteries; Bosch rolling out battery‑as‑a‑service for industrial equipment; and Saft announcing a joint venture to develop high‑temperature nickel batteries for mining applications.